Mitigation and insurance

By Richard Langdon; Samita Kaur, WTW

Published: 19 June 2023

Do you have cover?

What is mitigation from an insurance perspective?

Mitigation provisions in insurance policies are important when a problem or error arises which could prove costly to a business. It should be unsurprising that in this moment the questions of how to contain the problem, or how to stop it from turning into a crisis, arise.

From an insurance perspective, these questions may point you in the direction of mitigation cover under Professional Indemnity (PI) policies. Mitigating a loss is typically described as a payment made by an insured (including costs and expenses being potentially incurred) to investigate, prevent, mitigate, rectify, or compromise any ‘wrongful act’ (which may be defined under the policy), event, matter, or circumstance that could give rise to a loss/claim.

How can mitigation cover help in respect of trading errors? Insureds can look to seek indemnity for costs they may incur to correct an error before it develops into a crisis. Most importantly, eliminating the risk and cost associated with a third-party claim as well as protecting business interests is key to any risk management strategy. It may also be to the benefit of insurers as swift action can reduce the costs and potential liability incurred.

Mitigation and trading errors in the spotlight

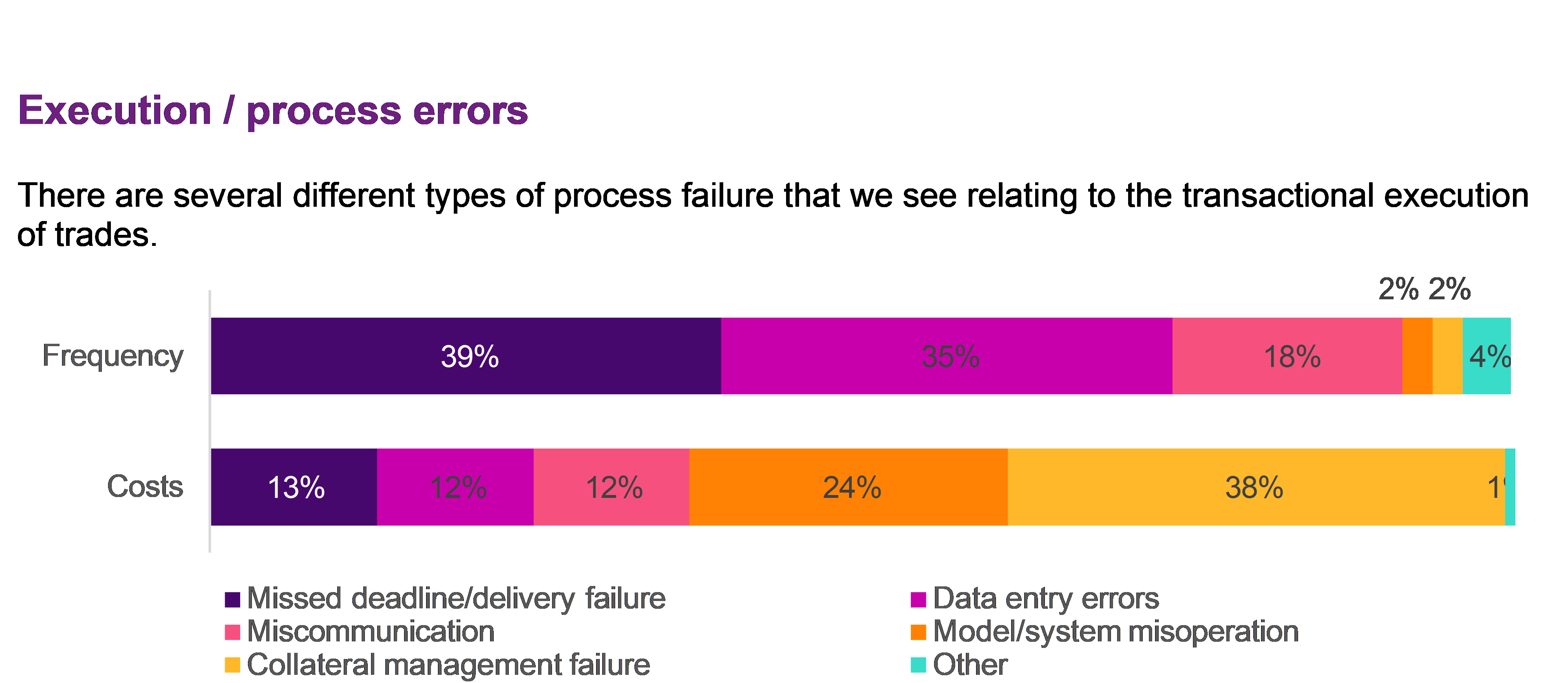

It is not unusual to see businesses having to explain the correction of a trading error to mitigate significant consequences, such as mass customer complaints, reputational damage and, most importantly, third-party legal action. There are many scenarios in which mitigation provisions can (subject to policy terms and conditions) provide cover. A review of WTW claims records illustrates that a scenario might include execution/process errors such as input and ‘fat finger’ errors, missed deadlines, miscommunication, and collateral management failures, each of which can result in significant losses that need to be avoided or corrected.

Errors can take shape in the form of an incorrectly categorised client in the system resulting in erroneous charges or the discovery of a hedging error, causing a loss to the fund and customers.

Mitigation cover in practice

In 2012, mitigation coverage was put into the spotlight as a result of a life insurer who made a payment of £100m into a pension fund to mitigate its risk of mis-selling claims. They looked to recover the payment into the fund under its mitigation provision. This went before the court as Insurers argued that it did not make the payment ‘in taking action to avoid a third-party claim’, but questioned whether the cash injection into the fund was done to protect the firm’s reputation and avoid the potential brand damage, rather than with the motive of avoiding or reducing a claim.1

The Commercial Court’s decision went in the life insurer’s favour and upon appeal by the Insurers, the Court of Appeal further upheld the Commercial Court’s decision that the policy in question did not apportion the coverage in this way and that as long as the payment was made to avoid or reduce third-party claims, and that they were of a type that would have been covered by the policy, the Insured’s motive was irrelevant.2

Separately, in 2020, an Investment Manager paid US$105 million after it discovered and corrected an error regarding the quarterly rebalancing of funds. In short, the Manager discovered there was a delay in rebalancing the funds which affected their value and therefore announced the US$105 million contribution to the Funds to compensate them for the performance difference that arose from market movements as a result of the delay.3 Although, it is unknown whether the manager was indemnified by their PI insurers, this is another good example of why mitigation coverage can be useful.

Insureds may want to consider their policy as to what coverage is available to them in these scenarios and to also take care to follow policy provisions in relation to notification.

Are these claims frequent?

WTW proprietary data demonstrates the frequency of trading error claims from 2007 to January 2023. We can see that for execution and process errors, there is a high frequency of claims in which the error involved a missed deadline/delivery failure. However, although these types of errors may be more frequent, the costs of the claims are typically low. In contrast, although collateral management failure claims are less frequent, when they occur, they are the costliest.

Model/system errors are also costly claims despite being less frequent. The data serves as a reminder to insureds that errors that may seem like a rare occurrence can prove costly and cause a more significant financial impact than other more frequent errors. Therefore, in these circumstances, mitigation cover becomes an important asset in crisis containment.

Conclusion

Insureds may come across scenarios or events similar to those discussed in this article in which they are faced with events or circumstances which require them to act quickly in the interests of crisis control for the business. As demonstrated, these decisions can prove costly and therefore it is important to incorporate a review of your insurance policy for coverage, as well as reviewing trade error and risk management protocols. Should mitigation coverage be available, Insureds should be mindful of any limitations as to what costs can be covered or potential preconditions that must be met, for example seeking the insurer’s prior consent before incurring mitigation costs.

1 Standard Life Assurance Ltd v ACE European Group – financial mis-selling claims

2 https://cms-lawnow.com/en/ealerts/2013/01/liability-insurance-court-of-appeal-upholds-first-instance-decision-on-apportionment

3 Invesco pays $105m in compensation after rebalancing errors on two US-listed income index funds