Implementing responsible investment at discretionary hedge funds

By Carol Ward, Man Group

Published: 21 March 2019

Introduction

Can hedge funds do good and do well at the same time?

As former US Vice President Al Gore puts it, “Outdated conceptions of fiduciary duty cannot be allowed to stand in the way of progress toward a better economic system. At stake is a low-carbon, prosperous, equitable, and healthy planet in which human civilization can flourish”.1 At Man GLG, we couldn’t agree more. Indeed, there are countless studies that demonstrate how hedge funds can do good and do well at the same time.

The more important questions, we believe, are how serious a hedge-fund firm is about responsible investment (‘RI’) – is it a box-ticking exercise, or is there a genuine culture of RI – and following that, how can a discretionary hedge fund successfully implement RI?

Demand on hedge funds to pay attention to RI is growing

RI is going to play an increasingly important part of a discretionary hedge fund’s investment decisions, as both allocators of money and governments alike place more emphasis on the topic.

The EU, for example, wants asset managers and other financial firms to disclose how they account for sustainability risks when allocating capital.2 The UN, aiming to “better align investors with broader objectives of society,” has proposed a due dilligence questionnaire for hedge funds as it tries to enforce its six principles of RI.3 According to research from AIMA and the Cayman Alternative Investment Summit (‘CAIS’), in May 2018, half of the 80 investment managers surveyed said that they had seen an increase in demand for RI from both current and prospective clients.

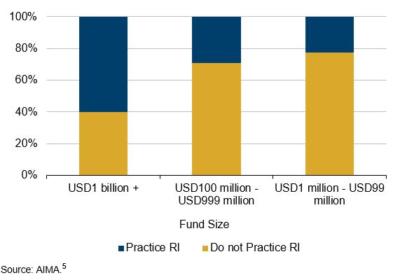

However, even with this increased demand for RI, there isn’t much of an appetite by hedge funds to engage in RI. According to a recent survey by AIMA and CAIS, only 60% of hedge funds with more than USD1 billion in assets are engaged in RI.4 This ratio dropped dramatically for both hedge funds with less than USD100 million in assets and those with assets ranging from USD100 million and USD999 million.

The opportunities of implementing RI at discretionary hedge funds

Traditionally, RI has been thought of something that long-only strategies can really implement. However, discretionary hedge funds that apply RI can do just as well, and we would argue even better, than long-only strategies.

1. The Ability to Go Short

One main reason why we believe discretionary hedge funds could do better than long-only strategies at implementing RI is because of discretionary hedge funds’ ability to go short the companies that are on the losing end of SRI or ESG factors.

2. Credit Opportunities

Governance is one of the most important factors to evaluate when investing in credit securities. Bondholders are looking to be repaid in full, and poor governance can easily jeopardize a company’s financial health, precipitating a rapid decline in the market price of the bonds and potentially impacting the final maturity and recovery value of the notes. Governance is also notoriously hard to score on an absolute basis or to model into traditional forward-looking credit metrics. At Man GLG, we tend to use a red-flag system where bond issuers that are flagged with poor governance are avoided.

3. Activism

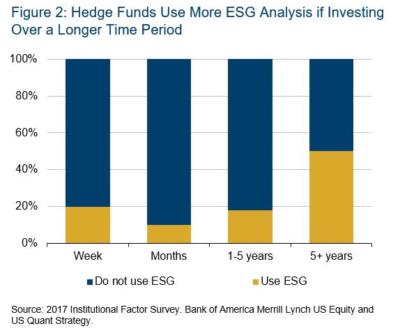

Discretionary hedge funds can be very active investors, which could result in positive outcomes if corporate engagement is done in a correct manner. In our experience, we have found that companies may be willing to have an open dialogue about where they need to improve on their ESG, SRI and/or sustainability metrics. It is, however, important to emphasize the importance of a fund’s investment time-horizon: a fund with a 5-year investment period, for example, may have more success when it comes to active management than a fund with a 3-month investment period. Indeed, it is widely acknowledged that ESG factors play a larger part in company analysis over longer time periods (Figure 2).

The challenges of implementing RI at discretionary hedge funds

However, RI at discretionary hedge funds is certainly not without its challenges.

1. Grey Areas

There are certainly grey areas when it comes to RI: Different funds many have different criteria as to what constitutes a good SRI, ESG or sustainable company. Additionally, how should a portfolio manager invest if a company is strong on ‘E’, but poor on ‘S’? There is also the age-old debate about divestment versus engagement.

2. The Lack of Data

ESG data have matured over the last decade, and we are entering a phase where the data have both a long-enough history and broad-enough coverage to make it interesting to quantitative investment firms. However, ESG data are qualitative, discretionary and unregulated. Indeed, the ESG data we obtained by vendors typically have a short history and is often retroactively collected. This is an area in which Man Group is applying its skillset – to improve the collection and analysis of ESG data. We believe that by spending the time to understand the nuances of each vendor’s methodology and properly handling their data quirks can potentially lead to a unique, alpha-generating dataset.

Implementing RI in practice

So, how can hedge funds implement RI in practice?

We believe the first and most important step is education: Portfolio managers need to own and embrace RI. To do that, education is required so that portfolio managers build an understanding of what clients expect and what it means to effectively integrate RI into the decision-making. Indeed, RI doesn’t have to be about ‘greening’ a portfolio, but rather weighing your portfolio toward companies that are proactively doing something about their sustainability issues.

Once portfolio managers understand the importance of RI, the next step is how to do the research on the companies. As mentioned earlier, a lack of data is definitely a challenge in implementing RI. However, this is improving: from sell-side integrating ESG factors into research to the aforementioned third-party service providers that rate companies based on how sustainable they are. Hence, portfolio managers do have a breadth of tools available to them when conducting research and analysis as it pertains to sustainability.

After decisions are made on which securities should be included in the portfolio – either as longs or shorts – discretionary portfolio managers have the ability to actively engage with corporate management to assess firm governance and potentially drive change. While corporate engagement is already a key part of the process of many discretionary portfolio managers, we believe portfolio managers should embrace active stewardship such as proxy voting. Larger hedge-fund firms tend to either have their own in-house stewardship teams or outsource this function.

In assessing stewardship activities at Man Group, we took a hard look at where our strengths and weaknesses lay and found that there was an over-reliance on service providers. This forced us to ask how we could make better decisions in proxy voting, especially as it related to RI. As a result, Man Group is in the process of developing an in-house stewardship team. The aim is that while we had previously been quite reactive when it came to stewardship, having an in-house team will help allow us to become more proactive.

Last but not least, quantifying responsible investment is key. Portfolio managers should be able to provide visibility on RI dynamics across portfolios. This could be as specific as metrics on carbon footprints across a fund’s portfolio, or as broad as exclusion lists.

What should asset owners look out for?

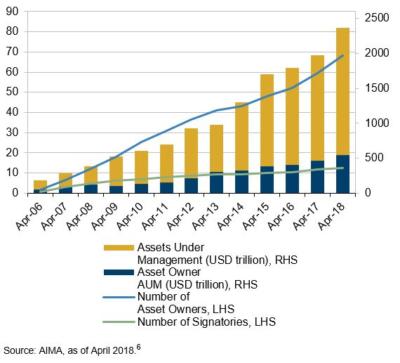

We believe the first thing asset owners should look out for is whether the hedge-fund firm is a signatory to the UN PRI. This is being increasingly expected from hedge-fund firms, as illustrated by the growth of signatories in Figure 3.

Once a firm has demonstrated a high-level commitment to RI, it may be worth digging a little deeper. RI at discretionary hedge funds can range from ESG analysis tacked on as an overlay to fundamental analysis, to ESG analysis being embedded into the fundamental analysis. If an asset owner is really passionate about RI, we believe it should take the time to really understand the discretionary hedge fund’s culture: portfolio managers must be able to demonstrate their commitment to sustainability, and be able to explain how they incorporate RI into their portfolio construction clearly.

One thing assets owners should bear in mind here is greenwashing, or the act of appearing to be ‘greener’ than the reality. It would be worth really doing the due diligence to determine whether RI is just a box-ticking exercise, or whether RI is really embedded in the fund’s culture.

We stress the ‘fund’ versus ‘firm’ here – It is quite difficult at firms with many funds to have a ‘one-size-fits-all’ approach. While there may be an overriding theme at a firm, different funds’ approaches may vary depending on the needs and interests of that fund’s clients, managers and strategy.

For example, Man Group has implemented a new RI Fund Framework, designed to establish a baseline requirement of ESG standards, and to provide credibility, clarity and consistency in Man Group’s approach to RI across its range of funds. There will be three categories into which all funds will fall: the base standard; a standard for funds with a further level of RI integration; and a standard for RI-dedicated funds. Under this framework, Man Group has formalised its mandatory, firm-wide exclusion policy on ownership of positions in companies that participate in controversial arms and munitions across all of its funds. In addition, Man Group is also introducing an RI Exclusions List, designating sectors that will be excluded from Man Group’s RI-integrated or RI-dedicated funds.

Conclusion

As RI becomes increasingly important to asset owners, governments and society in general, discretionary portfolio managers need to own and embrace ESG integration. At Man Group, our approach is to develop a ‘toolkit’ for portfolio managers to make it as easy as possible for them to integrate RI in to their existing process. After all, the long-term sustainability of the hedge-fund business requires forward-thinking environmental practices. The sooner we embrace it, the better.

Footnotes

1 https://www.unpri.org/Uploads/u/j/z/Fiduciary-duty---progress-report-2017.pdf

2 http://europa.eu/rapid/press-release_IP-18-3729_en.htm

3 https://www.unpri.org/pri/what-are-the-principles-for-responsible-investment

4 AIMA and CAIS collected 80 survey responses from hedge fund firms representing approximately $550 billion in total assets under management. Survey responses were collected from December 2017 to February 2018, and the results were published in June 2018.

5 From Niche to Mainstream: Responsible Investment and Hedge Funds.

6 https://www.aima.org/article/esg-integration-on-the-rise-and-how-to-implement-it-in-your-portfolio.html