Brave new world of price discovery - Adopters win, adaptors will need to catch up

By Vuk Magdelinic, Co-Founder and CEO, Overbond

Published: 27 January 2017

One of the most exciting and dynamic shifts in the financial world is the way that new financial technologies — ‘fintech’ — have penetrated various sectors within the market. The finance world is undergoing a dramatic shift experienced in other established industries (like publishing) that are built on information as opposed to concrete goods. Over the past decade, fintech innovation has influenced a range of sectors within the financial industry: payment technologies, wealth advisory companies, peer-to-peer lending, and consumer financing (to name a few). All these sectors have experienced substantial positive development due to technological innovation. In the similar fashion, the capital markets sector - although largely untapped - is a fertile ground for fintech providers to add value and to spur the types of innovation seen in other segments of finance. Tellingly, as KPMG noted last year, capital markets can only remain immune from fintech innovation for so long. “A perfect storm of conditions is brewing that makes financial technology the right solution for the right conditions at the right time,” they write. “And that time is now.”

The bond market - as the largest part of the capital markets - can benefit greatly from fintech innovation due to its structural conditions and recent market developments. The bond market is returning to a state of sustained growth, but struggling to meet the demand of investors, especially outside the cadre of institutional investors. 2016 has seen a sizable increase in U.S. bond supply: according to Bloomberg, 2016 had seen a 9.5 per cent increase by the end of August, surpassing $1 trillion in total new supply in September. While bond supply is rising, however, yields still remain low: over the course of 2016, yields have fallen consistently and only at the end of the year have we seen the indicators that yields will rise in the near future. And at the same time, liquidity in the secondary markets is down: in October 2015, large U.S. banks reported negative corporate bond inventories for the first time in history. Some Wall Street banks now hold a view that low market liquidity has become a norm for corporate bond markets.

Emerging fintech innovations promise to deliver solutions to many of the structural problems that exist in the market architecture for primary bond origination. Price discovery, for instance, is a vital aspect of market functionality that is fundamentally inefficient due to market fragmentation and a lack of suitable communication tools.

Because the market is functioning OTC (over-the-counter) and is fragmented - information flows slowly and unequally. Due to relative bargaining power and access to information, larger investors and dealers develop an inherent advantage in the marketplace. While this system works well enough for large institutional participants, it has the effect of exacerbating imbalances, whereby many investors — including those in emerging markets - are disadvantaged not only in terms of their opportunities to participate in primary bond issuances, but in their ability to navigate the process in such a way that allows for accurate price discovery. In effect, an unintended byproduct of a growing OTC bond market is that it has also grown to be filled with challenges and obstacles that raise costs and inhibit equal access for all investors.

The corporate bond origination process, largely done manually and only minimally updated over the last fifty years, is an impediment to the efficiency of price discovery and diversification of the entire bond market — two of the biggest challenges that the market faces for long-term sustainable growth. Even in an increasingly transparent, information-focused financial environment, the bond market remains opaque; what information is readily available is often fragmented and spread thin between different players in the marketplace. Investing power is thus thrust into a state of imbalance: smaller investors do not have neither the time nor the resources to accurately engage in price discovery and determine transaction costs — which, for smaller investors and smaller transactions, can be up to twenty times higher than for their larger counterparts. Increased costs, and the increased difficulty of accurate price discovery, enable only the largest institutional investors to meaningfully participate in the primary bond market. This, in effect, keeps the market from diversifying in a way that would promote sustainable growth.

It also contributes to a lack of connectivity between dealers, investors, and issuers who in the bond market (as opposed to equity markets) have no centralized infrastructure through which to buy and sell and thus lack the kind of robust data and analytic tools to streamline price discovery. It is possible to solve many of the problems inherent in price discovery at the point of bond origination, however. By using technology to increase transparency, connectivity, and the flow of information, fintech platforms can solve both problems: first, they can serve as a centralized system through which dealers, issuers, and investors can interact and connect; secondly, by increasing transparency and connectivity, fintech platforms can drastically improve the accuracy and efficiency of price discovery, information flows, and deal execution, thus improving some of the major obstacles to efficient bond origination.

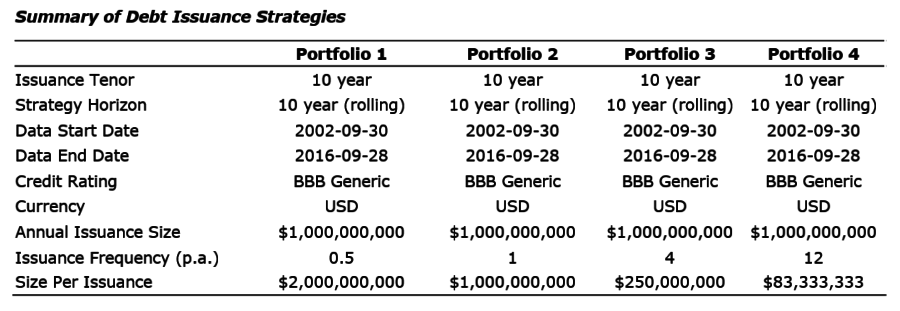

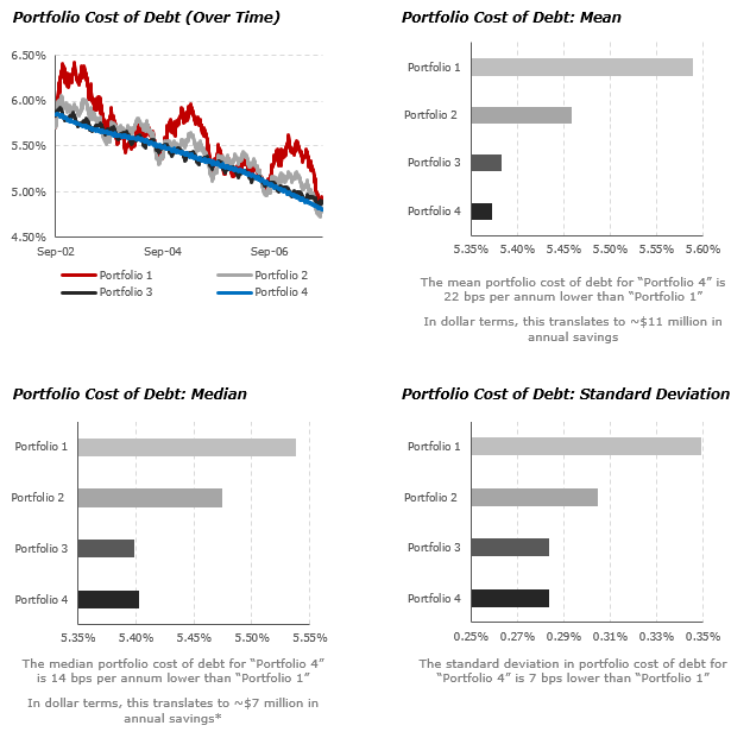

Interestingly, as our own fixed income research shows, if major obstacles related to the current nature of bond origination are overcome through fintech innovation, substantial benefits to issuers, investors, and dealers are possible. The ability to issue debt more frequently is hampered primarily by the costly and manually intensive bond issuance processes that all market participants have relied on for decades. A less manually intensive, more transparent, and connected issuance process would allow dealers to reduce deal related transaction costs while streamlining price discovery for all market participants. As a result, issuers would be capable of accessing the market on a more frequent basis and for smaller notional amounts – allowing for opportunistic issuances. Based on our fixed income research, the ability to issue more frequently and in smaller notional amounts would drive down the cost of funding for issuers while reducing interest coupon volatility (Exhibits 2, 3, 4, and 5). Conversely, with more frequent issues, both large and small investors would have more opportunities to participate in the bond issuance process, potentially driving more equality in new issue participation.

he capabilities of fintech have proven to be a valuable asset to other financial sectors, improving efficiency, lowering costs, and increasing the breadth and diversity of the user base. The bond market, as it exists now, is in need of modern solutions and processes. Technological solutions are the optimal way to solve the most pressing problems in capital markets: a lack of centralized connectivity, the difficulty of price discovery amidst a volatile economic climate and the challenge of diversifying the investor base. With fintech innovation the bond market can bring itself towards a more efficient, centralized and diverse future.

To contact the author:

Vuk Magdelinic, Founder and CEO at Overbond: [email protected]