Fed’s challenges as it seeks a neutral monetary policy

By Blu Putnam, Chief Economist , CME Group

Published: 13 July 2018

The Federal Reserve (Fed) now appears determined to seek a neutral monetary policy. It is raising rates and shrinking its balance sheet as it unwinds the Bernanke-era emergency policies of the Great Recession. So far, this well-telegraphed approach to unwinding quantitative easing (QE) and raising rates has had no discernible impact on the pattern of real GDP, inflation or the labour markets. The next task is finding the neutral gear for interest rate policy, which may not be as easy as it might sound. Even the definition of a neutral interest rate policy is not so clear and depends on one’s views on inflation. In addition, one is led to an important examination of how to enforce a given short-term interest rate target. In turn, a discussion follows on the way the Fed pays interest on reserves which puts an emphasis on the inadequacies of the federal funds rate as the primary policy target rate. It is going to be a very interesting debate.

What is Neutral?

Immediately after the September 2008 financial panic triggered by the Lehman Brothers bankruptcy and the AIG bailout, the Fed quickly lowered the effective federal funds rate to close to zero. For the full six years between 2009 and 2014, the effective federal funds rate averaged just 0.13%. The first rate rise came in December 2015, and then the Fed got cautious and delayed the next rate increase until December 2016. Since then, the Fed has been on a steady pattern of “skip an FOMC meeting, raise rates, skip a meeting, raise rates,” wash, rinse and repeat.

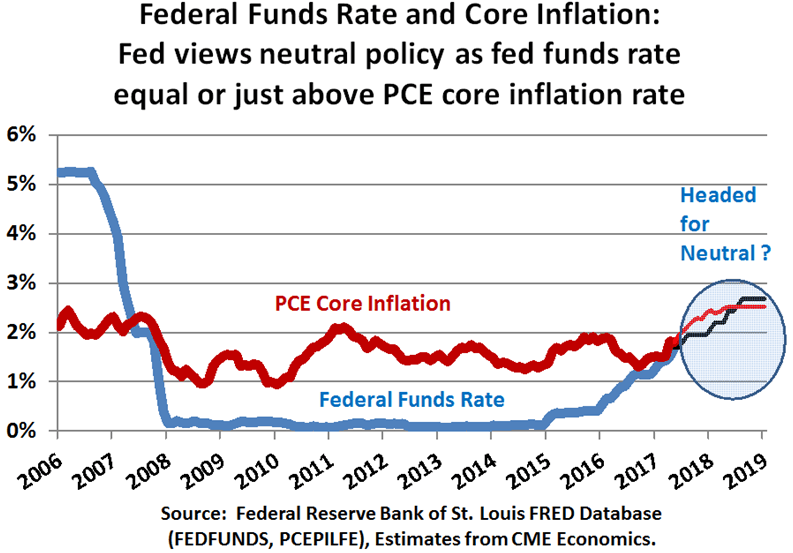

The Fed now seems on a path to steer the effective federal funds rate to a level that is equal to or just modestly higher (25 to 50 basis points) than the prevailing rate of core inflation, which we take to be the Fed’s new definition of a neutral short-term interest rate policy. Of course, the definition of a neutral policy is not universally agreed. Pre-2008, the prevailing view was that a neutral policy reflected an inflation risk premium of maybe 2% above the prevailing core inflation rate. The Janet Yellen view was that the neutral inflation risk premium was now close to zero or just incrementally positive, and that view appears to have been accepted by many FOMC members.

Then, there is the issue of estimating the path of inflation. If the FOMC members’ collective wisdom on inflation develops as estimated, then core inflation might rise to 2.5%. The Fed remains extremely data dependent, so if the inflation path changes, one can count on the anticipated rate path being changed as well.

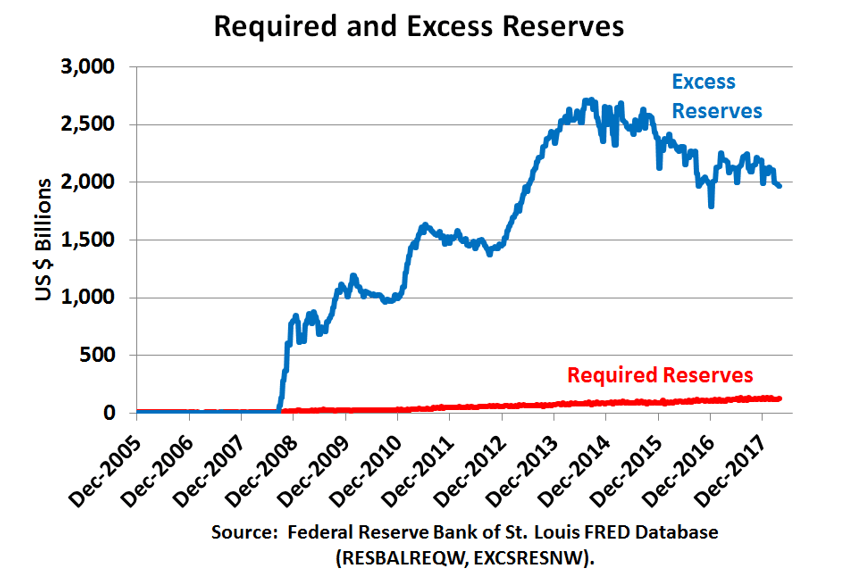

Figure 1.

The Shape of the Yield Curve matters, too

The story, however, gets much more complicated. One constraint on the Fed’s rate rise ambitions is the yield curve’s shape. Flat or inverted yield curves historically have been excellent predictors of both coming equity volatility and future recessions. A flat or inverted yield curve indicates the Fed has gone too far and pushed rates too high. It has only taken six decades of history for the Fed to elevate this statistical correlation into the rate policy debate. And, who knows? The yield curve may not be applicable this time around, but the Fed is paying the shape of the yield curve considerable attention. If bond yields do not rise in parallel with short-term rate increases (that is, a flattening yield curve), the Fed most probably will delay future rate increases while it observes inflation data and bond market activity.

Enforcing the Fed Funds Target and Payment of Interest on Reserves

The Fed currently enforces its federal funds rate target range by paying interest on reserves it holds at the upper bound of the target range. The Fed only started paying interest on required and excess reserves at the end of 2008 as part of its emergency response to the 2008 panic. By paying interest on reserves at the ceiling of the new approach to setting a federal funds target range, the Fed was effectively providing a very nice income stream with no credit risk to the banking system in 2009 when it really mattered.

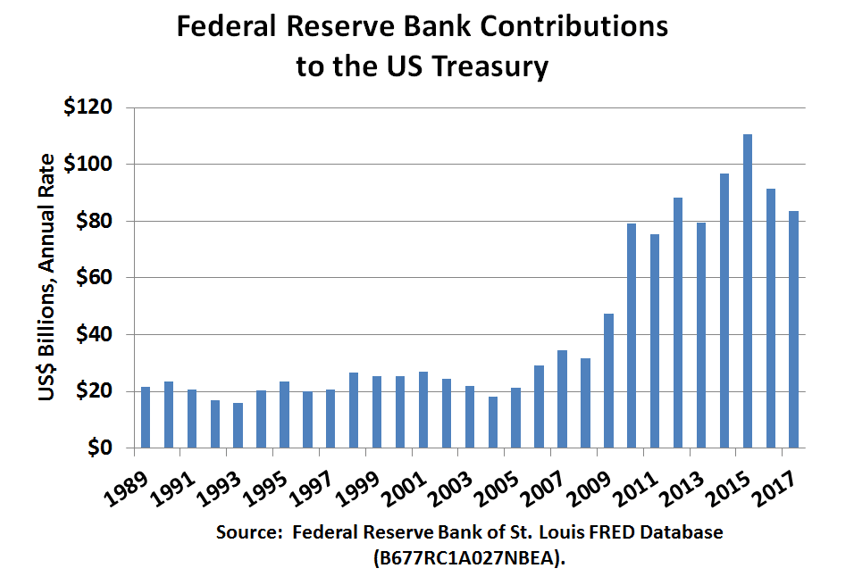

As short-term rates have been pushed higher, the Fed has increased the interest rate it pays on required and excess reserves in lock step with increases in the federal funds target range. This works to increase the Fed’s own costs of funding its balance sheet and serves as a drag on the Fed’s earnings, most of which are paid to the U.S. Treasury. Even with incrementally rising short-term rates, the Fed is in no danger of losing money. Prior to 2008, the Fed typically contributed around $20 billion or a little more to the U.S. Treasury each year. Once QE ramped-up the Fed’s balance sheet, annual contributions in the 2013-2017 period soared to the $80-$100 billion range. The Fed’s earnings are now expected to decrease modestly year-on-year as rates rise further and as the Fed shrinks its balance sheet and holds fewer assets.

Figure 2.

As Fed earnings decline with higher rates and a smaller portfolio, we expect the Fed to evaluate different ways of exerting influence over short-term rates to break the link between the payment of interest on reserves and decisions to encourage short-term rates to move higher or lower. This possibly means the Fed may consider moving away from federal funds as the target for Fed interest rate policy.

Before the 2008 crisis and subsequent expansion of the Fed’s balance sheet, excess reserves were much smaller. It was not uncommon for banks that had strong corporate lending franchises and weak core deposit bases to need to borrow reserves to meet their reserve requirements. Similarly, banks with a strong consumer deposit base would have an excess of reserves over their requirements, and they would lend federal funds (deposits with the Fed) to banks in need of reserves to meet their requirements. By using repurchase (repo and reverse-repo) transactions the Fed could temporarily add or withdraw reserves (fed funds) from the banking system and influence the federal funds rate – the overnight rate at which one bank lent its deposits at the Fed to another bank.

Figure 3.

Once excess reserves ballooned after 2008, few banks needed additional funds to meet their reserve requirements. And, Fed repo transactions that added or withdrew excess reserves made little difference since the overhang of excess reserves was so large. While the Fed still does (reverse) repurchase agreements, the impact on the federal funds rate is fleeting at best. The primary means of enforcing a higher target range for the federal funds rate has been to raise the interest rate paid on reserves to the target range’s ceiling. If a depositary institution needed to borrow federal funds, it would pay a discounted interest rate or higher price for the federal funds. The result is that federal funds have tended to trade very steadily (except for the last few days of any given month) at around 7 – 13 basis points (annual rate) lower than the ceiling, which has kept the federal funds rate comfortably inside the target range. The volume of transaction, however, is generally not very high – around $75 billion a day in April 2018, for example.

The point is that the federal funds rate no longer trades as a truly representative rate for overnight lending. If the Fed chose a new broader-based and much more representative rate to target, then the Fed would gain the freedom and flexibility to set a rate of payment of interest on reserves that might be lower than the new target short-term interest rate.

Will the Fed eventually choose to target some other rate than federal funds? We do not know. We do know that there are very strong incentives in place in the post-2008, post-QE environment to consider replacing the target rate with something more representative of market conditions than federal funds. And we also believe the Fed may very well see advantages in delinking its target rate from the interest rate it sets to pay on reserves. We expect the debate within the FOMC to commence very soon, although it may last a year or more. There is considerable research to be done. To paraphrase the former member of the Bank of England’s Monetary Policy Committee, Charles A. E. Goodhart, “when a central bank targets a specific metric, the nature of the metric is forever changed”. This observation in various forms is now known as Goodhart’s Law and can be viewed as a derivative of German theoretical physicist Werner Heisenberg's uncertainty principle. It provides a cautionary message, yet our view is that change is coming for Fed rate targeting and for how interest is paid on reserves and change may come sooner than one might expect, given that the debate has yet to commence.

To contact the author:

Bluford Putnam, Managing Director & Chief Economist at CME Group: [email protected]

Disclosure

All examples in this report are hypothetical interpretations of situations and are used for explanation purposes only. The views in this report reflect solely those of the author and not necessarily those of CME Group or its affiliated institutions. This report and the information herein should not be considered investment advice or the results of actual market experience.