MiFID2 and trade reporting: Get ready for big changes

By Kirston Winters, MD & Co-Head of Product Management for MarkitSERV and Brie Lam, Director, Regulatory & Compliance Services, IHS Markit

Published: 21 January 2018

MiFID came into effect in 2007 – under the current regime, buyside firms are typically not required to publish trades and real-time public reporting (“trade reporting”) is handled by trading venues and dealers.

However, in January 2018, MiFID2 rules will shift the responsibility for trade reporting to the buyside for certain products and in certain situations.

The trade reporting rules are complex and, as the implementation of MiFID2 approaches, asset managers are justifiably confused and concerned – and if they’re not, they should be.

The new challenge for asset managers stems from a creation unique to MiFID: the systematic internaliser (SI). Under MiFID, an SI is defined as an “investment firm which, on an organised, frequent, systematic and substantial basis, deals on its own account by executing client orders outside [a trading venue].” In layman’s terms, it’s any firm that matches and fills a significant number of client orders internally.

But wait, there’s more: MiFID2 changes how SIs are designated. A firm could be an SI in hundreds of instruments and not in hundreds of others. For off-venue trades, where both parties are EU firms, if just one party to a trade is an SI, it is responsible for trade reporting. If neither party to the trade is (or both are) an SI, then the seller is responsible for trade reporting.

The rub is keeping track of it all and reporting within minutes if it’s your obligation.

Trade reporting mandate

As mandated by MiFID2, for every transaction subject to “traded on a trading venue” (ToTV), whether traded on-venue or off-venue within the EU, trade reporting must be conducted as close to real-time as possible; the trade must be reported by just one of the parties involved, whether it is the trading venue itself, an SI or an investment firm. ESMA defines the time window within which to report as one minute post-trade for equities and equity-like instruments, and 15 minutes for other instruments (reducing to five minutes after three years). Depending on the instrument, up to 33 data fields are required to be reported by the Approved Publication Arrangement (APA).

Failure to report is not an option, but neither is duplicative reporting by both parties to a transaction. How do firms know who has the obligation to report if they don’t know if their counterparty is an SI in that instrument?

Redefining systematic internalisers

Under the original MiFID, the SI regime was limited to equities transactions, but MiFID2 expands coverage to include virtually all instruments. The most drastic change in the regime, however, is that quantitative thresholds for the determination of SI status have been defined at the sub-asset class level. Under MiFIR, Regulation No. 600/2014 drafted to accompany MiFID2, the SI thresholds are defined as a percentage of total trading activity in the EU, with ESMA publishing the aggregated instrument volumes quarterly. A firm exceeding the thresholds for a product is an SI for that product and is obligated to adhere to all regulatory requirements that accompany that status.

This means a firm can be deemed an SI for USD-EUR cross currency swaps (2-3 years), but a non-SI for JPY-USD cross currency swaps (2-3 years) and a non-SI in USD-EUR cross currency swaps (3-4 years). Thus, each firm will need to assess their SI status at granular levels across all asset classes.

Furthermore, the SI status of a firm is dynamic and they must reassess based on updated thresholds and volumes published by ESMA, even firms that don’t breach the thresholds in a certain product can still opt to be an SI.

So, what does all this really mean?

In a traditional off-venue sellside versus buyside transaction, one might expect the dealer to report; however, if the dealer is not an SI in a particular instrument and the buyside counterpart is the seller then it becomes the obligation of the buyside to report the trade within the 15-minute window. Being able to meet that obligation implies that the buyside has the operational and technological processes in place to transmit requisite data to an APA, including all mandatory reportable attributes for that trade.

Trading only with SI firms in an attempt to avoid reporting requirements is unlikely to be allowed as that will not satisfy the best execution requirements under MiFID2.

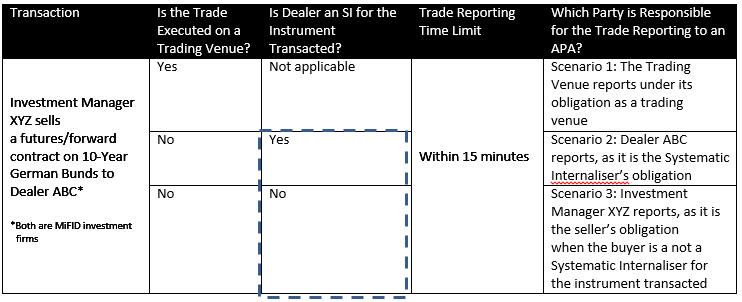

The chart below illustrates how the obligation to report trades is determined.

Chart: Whose obligation is it to perform the Trade Reporting?

Communication of SI Status to the Buyside

If an asset manager (non-SI) is obliged to report when selling to another non-SI, they will need to know whether their counterparty is an SI for every off-venue trade. ESMA will publish a firm’s status as an SI – but it does not plan to publish information at the instrument level. So you will know whether your counterparty is designated as an SI in something, if it listed on the ESMA register but not whether it is an SI for the instrument you just traded. This adds another significant layer of operational complexity for the buyside: every minute of every day, the firm will need to know whether it is the party obligated to report trades to an APA.

That’s a lot of extra work.

The good news: IHS Markit can provide granular-level SI status information on counterparties and help automate part of the reporting process. Just like it does for so much other information governing the relationship between dealers and asset managers, the Counterparty Manager platform can serve as a central hub for dealers to store data on which instruments they are designated as SIs and permission their clients to access it in order to help them understand their reporting obligations.

Concluding Thoughts

MiFID2 places significant burden on buyside firms to understand the SI status of all their counterparties at a granular instrument level, and to be able to report trades to an APA in a timely manner when — and only when — obligated to do so. With the compliance date approaching, the time is now for asset managers to ensure they are prepared to determine their counterparty’s SI status by instrument and to plan how they will access an APA, via vendor solution or internal build.