Private fund side letters: common terms, themes and practical considerations

By Christopher Gardner and Mikhaelle Schiappacasse, Dechert

Published: 18 January 2019

Introduction

Side letters are an (increasingly) common way of formalising negotiated arrangements between a private fund and an investor.1 Whilst used more widely in the closed-ended fund context (given the limited withdrawal rights associated with such funds, the typically higher level of negotiation and greater structural complexity), they are also a feature of open-ended funds, for instance where there is a seed or cornerstone investor investing significant capital or an investor subject to specific tax or regulatory regimes that require bespoke terms.

A side letter supplements and, where the fund takes contractual form (such as a partnership), can override the terms of the fund’s constitutional documents and is typically required where an investor has specific commercial, legal, regulatory, taxation or operational concerns with respect to its investment in the fund. In many instances it is easier to agree concessions in these separate agreements rather than amend the fund’s constituting documents (being the private placement memorandum and the constitutional documents such as the partnership agreement or articles), especially as the latter approach would mean the rights agreed would generally then be available to all investors. Some rights are also most practically recorded in a side letter (for example confirmation of an advisory committee seat for a closed-ended fund).2

This article provides an overview of common side letter terms and current themes in the private fund market. It also considers the regulatory context and practical points for managers navigating the restrictions and obligations of multiple side letters.

Common terms

Most favoured nations ("MFN") rights

Where a manager is willing to provide an MFN right, these rights are generally reserved for more significant investors as they can have wide-ranging implications for the fund, especially if they are not managed effectively.

An MFN right allows an investor to elect to receive the side letter provisions negotiated by other investors.3 However, MFN provisions can be drafted in a number of ways, meaning that what the investor may actually be entitled to elect to receive can vary widely. For example, the drafting may vary in respect of: (i) whether the MFN applies to all side letter provisions or just, for example, to the fee provisions, (ii) the MFN only applying in respect of those provisions negotiated by other investors with an equal or smaller investment in the fund (typically affiliated investors will be aggregated), and (iii) whether the investor can see all side letter provisions negotiated (regardless of whether it is allowed to elect to receive them) or just those it may elect to receive. It is also common to carve out certain terms from the MFN, for example, rights granted to first closing or seed investors, rights granted due to an investor’s specific legal, regulatory or taxation concerns and the right to an advisory committee seat. However, even with careful drafting, an MFN right can significantly extend the fund’s (or the manager’s) obligations; managers should therefore carefully consider which investors’ terms are likely to be captured by the MFN when negotiating these (and other) side letter provisions.

Transfers

Transfer rights are particularly relevant in the closed-ended fund context where an investor cannot redeem from the fund should it wish to. Managers negotiating side letters on behalf of a fund should ensure that a transfer right provides them with sufficient comfort with respect to the identity and nature of the transferee (this is particularly the case where the fund has a credit facility and does not want to jeopardise its borrowing base) and that appropriate customer due diligence information will be provided in connection with any transfer. A blanket consent is therefore not advisable. Transferability is particularly important to certain investors, for example certain German pension funds,4 who may need to be able to demonstrate free transferability (or as near to free transferability as the fund can practically offer) for regulatory reasons.

Excusal rights

The constitutional documents of closed-ended funds typically include a mechanism whereby an investor can be excused from participating in particular types of investments (generally due to regulatory or other internal constraints). Often an investor must notify the fund of any restrictions before it invests and/or require the opinion of external legal counsel to confirm that it is so restricted. If a fund is willing to negotiate excusal rights, it should try to limit the amount of investor discretion in determining what an excused investment is as the emphasis should be on using the investor’s full commitment rather than allowing it to cherry pick deals. If the scope of the prohibited investments is stated in the side letter itself, it is generally helpful to state why they are prohibited in order to increase the chance that the provision is taken outside the scope of any relevant MFN right.

Enhanced reporting and information rights

These side letter requests can come in many guises, including requests to vary the frequency, format and content of reporting. Some investors may have genuine tax related concerns (for example, the need to be supplied with K-1 schedules in order to prepare their US tax returns) or regulatory reporting issues (such as the need to comply with the Solvency II Directive (2009/138/EC)). Any such terms should be both commercially appropriate and operationally practical for the fund and its manager. For example, a request for portfolio level information should not result in the investor holding information it could use to its competitive advantage or to the detriment of other investors. This is an area of particular sensitivity in the open-ended fund context where portfolio level information should generally only be provided when stale, e.g., after further trading of the portfolio so that its then-current composition is not selectively shared.

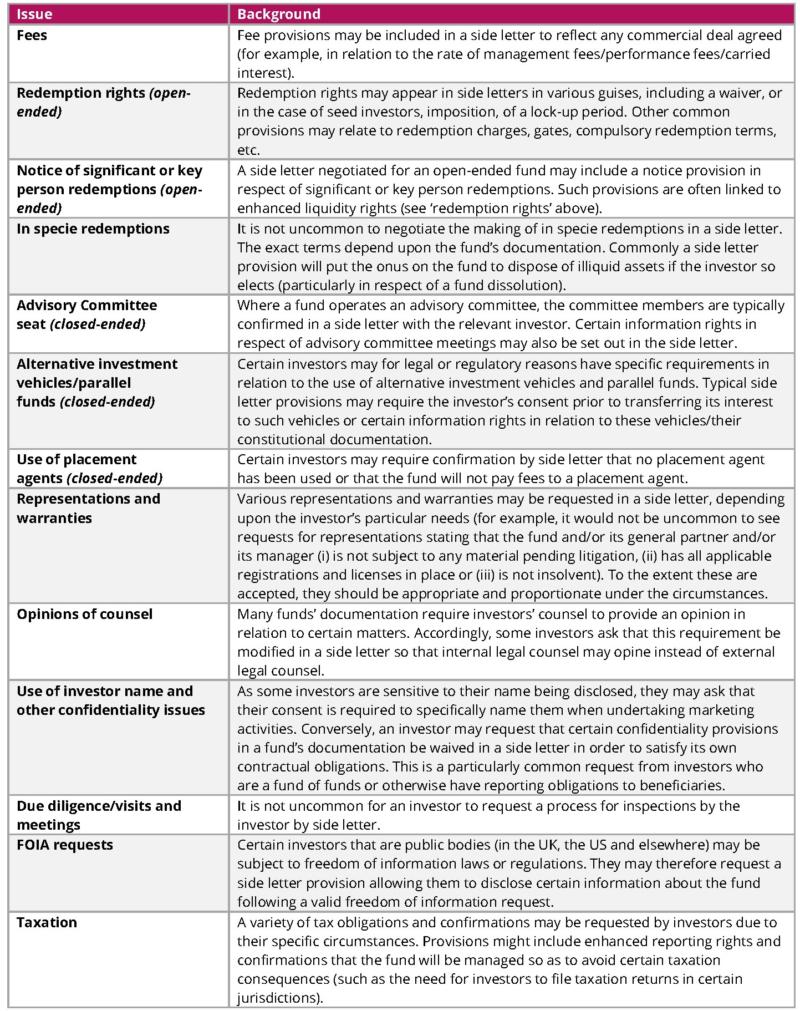

Other common provisions

The table is a summary of common side letter requests. Whether it is appropriate to grant such requests should be considered on a case by case basis.

Themes

Set out below are some current themes that are relevant to negotiating side letter terms.

Co-investments and other alternative ways of investing

In recent years there has been growing interest in co-investment vehicles, separately managed accounts and other alternatives to classic commingled funds. While investors commonly seek an acknowledgement in a side letter that they are interested in co-investment opportunities (or a similar election right), the range of alternative investment structures currently in vogue introduces new side letter concerns, particularly in relation to strategy and allocation issues (for example strategy caps and successor fund provisions). Typically it is more appropriate for the manager rather than the fund to sign up to these requests. If these issues arise, managers should ensure that the concessions are achievable, do not unduly limit their firm’s growth and development strategy and that they can be effectively monitored.

Use of credit facilities

Credit facilities are an increasingly popular tool used by closed-ended funds to satisfy short-term bridging needs and smooth the capital call process. However, they pose certain distinct issues with respect to side letters which can be problematic, particularly where the lender’s ability to take security is compromised or the borrowing base is otherwise restricted. Examples of this include where excusal or transfer rights affect the existing credit assessment on the borrowing base.

To the extent a fund has a credit facility and any of the provisions described above are also covered by an MFN right, these issues can be exacerbated because multiple investors may be able to elect to receive the problematic provisions. Managers may therefore wish to include a carve-out in their standard MFN clause in respect of side letter provisions which affect the fund’s credit facility.

Key person issues

Key person terms are common in the closed-ended fund context (where a key person event is likely to trigger the suspension of the investment period). Their use in the open-ended funds context is increasing, particularly to tie in certain key persons financially, including required investment levels and notification rights where a key person submits a significant redemption request (which could potentially be linked to favourable liquidity rights). Provisions regarding no bad acts are also common, especially in seed arrangements or where significant investments are made and are often particularly relevant for smaller managers where the conduct of a key person is more likely to impact performance of a fund.

Pooling of UK local government pension schemes

Certain UK local government pension schemes have recently pooled their investment assets into eight distinct pools to improve the efficiency of the management of their assets. From a side letter perspective, this effectively increases their negotiating power, particularly if one of the schemes is granted an MFN which is extended to all members of its pool. However, the schemes have not pooled using a consistent structure so, as it stands, requests should be considered on a case by case basis – it may be that the various schemes do not necessarily fall within a fund’s definition of affiliate (which is generally how entities are grouped together for the purposes of an MFN clause). The pooling of these entities continues to evolve and a standard approach may develop over time.

Environmental, Social and Governance ("ESG") concerns

Investors are increasingly looking to funds to make ESG commitments with respect to their investments. ESG provisions may include a confirmation that the fund will comply with the UN Principles for Responsible Investment when making investments or that investee companies comply with the ten principles of the United Nations Global Compact or other guidelines that are more specifically tailored to the investor in question, including restrictions on making investments in companies engaged in certain lines of business. If such a provision is contemplated by a fund, it should ensure it is able to comply with these provisions and, from a practical perspective, to provide any reporting agreed.

Regulatory context

Aside from the commercial and practical considerations relevant to agreeing to a side letter provision, there are certain regulatory issues that managers should also bear in mind.

Managers that are subject to the Alternative Investment Fund Managers Directive (2011/61/EU; "AIFMD") (whether as a European Economic Area ("EEA") based alternative investment fund manager ("AIFM"), managing an EEA alternative investment fund ("AIF") or through marketing an AIF to investors located in the EEA) must comply with the AIFMD rules on preferential treatment. Under the AIFMD, investors must be provided with a "description of how the AIFM ensures a fair treatment of investors and, whenever an investor obtains preferential treatment or the right to obtain preferential treatment, a description of that preferential treatment, the type of investors who obtain such preferential treatment and, where relevant, their legal or economic links with the AIF or AIFM." This disclosure obligation applies prior to investment and following any material changes to such preferential treatments. The introductory recitals of AIFMD also require that any preferential treatment is disclosed in the AIF’s rules or instruments of incorporation – this can be achieved through broad disclosure in the private placement memorandum or partnership agreement (although some managers prefer to include more tailored terms to ensure investors are not provided with too much of a 'shopping list'). The ability to request further information from the manager is also commonly included in the private placement memorandum, with summaries of side letter rights typically made available.

EEA based AIFMs are also subject to an additional requirement to ensure the fair treatment of investors. In particular, any preferential treatment accorded to one or more investors must not result in an overall material disadvantage to other investors. EEA managers should bear this requirement in mind when deciding whether to agree to a particular side letter provision.

From a U.S. Securities and Exchange Commission ("SEC") perspective, there is concern about an investor being given preferential treatment in a side letter that may have a negative impact on other investors, such as preferred liquidity and information rights. However, such provisions may be acceptable if sufficiently disclosed to the other investors who are able to take the information into account when making their investment decision. The more acute the conflict or significant the potential impact on other investors, the more detailed and extensive the disclosure should be. The SEC staff on examination has been known to review side letters to test whether they are being adhered to and whether proper disclosure was made. Deficiencies in this area can result in negative written findings at the conclusion of an examination and, in sufficiently serious cases, could result in an enforcement referral.

Practical Considerations

Below are some practical considerations that could be relevant when managing a fund with side letters:

- Side letters supplement the terms of a fund’s constituting documents, so they should be considered whenever these documents are consulted.

- It is better to be consistent in agreeing side letter terms, for example, having a 'house' provision that is stuck to. This allows continuity of application.

- Managers with a number of side letters should consider keeping a centralised record of all side letters agreed for the fund, allowing compliance to be monitored on an ongoing basis. Annual (or more frequently if appropriate) certifications from the teams responsible for compliance with individual provisions can support this process.

- Managers managing open-ended funds can simplify monitoring and compliance by keeping a clear record of when an investor has redeemed (such that the side letter is no longer relevant).

- While it is tempting to immediately move on to the next project after a closed-ended fund’s final closing, it is important to ensure the MFN exercise is handled immediately in order to avoid any technical breaches. The MFN exercise ensures that all investors who are allowed to see/elect to receive other investors’ side letter provisions are presented with their options within the agreed timeframe. This is typically achieved through an election form and can take some time to coordinate if a significant number of side letters are involved and/or if a complex set of carve outs apply. The need for consistency between side letter terms (including any MFN rights granted) becomes particularly apparent when conducting this exercise.

Conclusion

Side letters are becoming an increasingly significant part of a fundraise. Managers should be alive to the implications of agreeing to side letter provisions, considering each term from a commercial, legal, regulatory and operational perspective. Issues are amplified where any MFN rights are involved. The themes identified in this note also demonstrate that the private fund space continues to evolve and that managers also need to adapt in order to ensure that they move with the times, rather than getting caught out by a term that is hastily agreed to without the overall implications receiving proper attention.

This document is not legal advice and should not be relied on as such. Parties to a side letter negotiation should seek advice on the particular transaction in light of their circumstances.

Footnotes

1. In certain circumstances the manager may also be a party. As a general matter, to avoid any enforceability issues, care should be taken to ensure that the correct parties are parties to the side letter and in the right capacity. For example, there have been cases in the Cayman Islands where it has been held that a side letter is not enforceable because the beneficiary rather than the registered interest holder was a party to a side letter and because a manager had entered into a side letter on behalf of the fund (and did not have sufficient authority to bind the fund).

2. Conversely, certain rights generally should not be included in a side letter, notably those that would create a new class of interests from a local law perspective or restrict the fund as a whole (such as tighter investment restrictions than those described in the fund’s constituting documentation).

3. In some circumstances an MFN is included in the fund’s constituting documentation rather than being agreed separately by side letter.

4. These are commonly referred to as so-called ‘VAG’ investors, i.e., those which are either a German insurance company, pension pool, pension fund or other pension scheme which is directly or indirectly subject to the provisions of the German Insurance Supervision Law or the Ordinance on the investment of restricted assets of pension schemes, funeral expenses funds and small insurance companies or the Ordinance on the investment of restricted assets of pension funds regarding the investment of their restricted assets.